⚡ Storm or Roof Damage? Get a FREE Estimate

Text ESTIMATE to (844) 907-2546

Or call (800) 792-0212 for 24/7 emergency response

AI-powered • No obligation • Licensed IL & WI

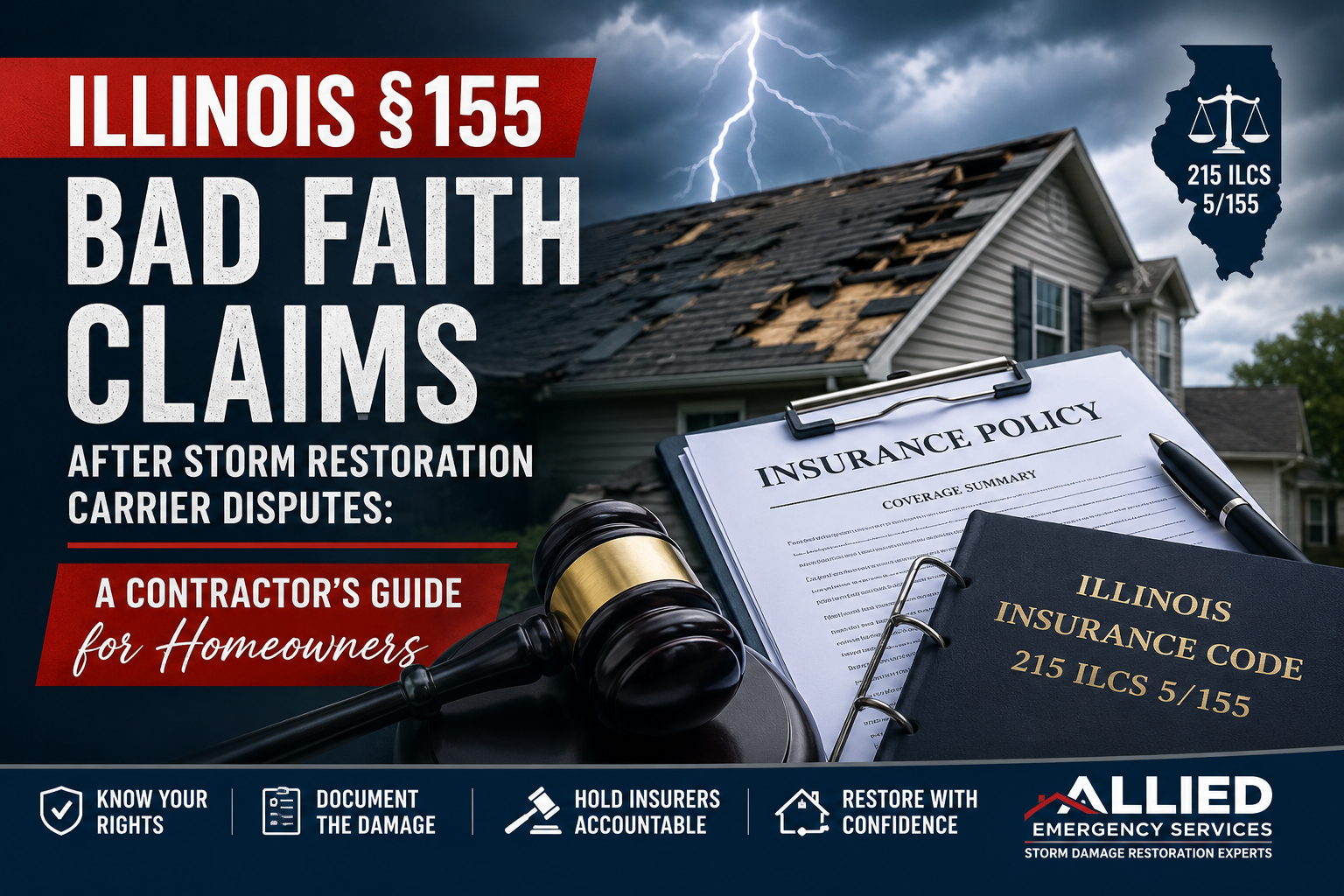

Direct Answer: When Can an Illinois Storm Insurance Dispute Become a §155 Bad Faith Issue?

In Illinois, a storm restoration insurance dispute may become a 215 ILCS 5/155 issue when an insurance carrier’s claim delay, denial, or underpayment appears vexatious and unreasonable. Homeowners often call this “bad faith,” but Illinois law commonly analyzes these disputes under Section 155 of the Illinois Insurance Code, not as a simple standalone “bad faith” lawsuit.

Under 215 ILCS 5/155, a court may award taxable costs, reasonable attorney fees, and a statutory penalty when there is an action involving the insurer’s liability under the policy, the amount of loss payable, or an unreasonable delay in settling the claim, and the insurer’s conduct appears vexatious and unreasonable.

For storm restoration claims, §155 may become relevant when a carrier delays payment, ignores documented storm damage, refuses to evaluate code-required repairs, fails to pay undisputed amounts, or repeatedly rejects a properly supported roofing, siding, gutter, water damage, or structural restoration supplement without a reasonable basis.

However, §155 is not automatic. Illinois courts generally consider the totality of the circumstances. A genuine coverage dispute, pricing dispute, causation dispute, appraisal issue, or policy interpretation issue may prevent a §155 award if the carrier had a reasonable basis for its position.

Illinois §155 Quick Facts for Storm Damage Homeowners

| Question | Answer |

|---|---|

| What law applies? | 215 ILCS 5/155, part of the Illinois Insurance Code. |

| What conduct matters? | Vexatious and unreasonable claim delay, denial, underpayment, or settlement conduct. |

| Is every denied storm claim bad faith? | No. A legitimate dispute is not automatically vexatious or unreasonable. |

| Who decides §155 penalties? | The court, not the contractor. |

| Can a contractor prove the facts? | A contractor can document damage, scope, code issues, pricing, photos, measurements, and communications. |

| Can a contractor give legal advice? | No. Homeowners should consult an Illinois insurance attorney for legal advice. |

| Why does this matter after hail, wind, or tornado damage? | Carrier disputes often involve causation, matching, code upgrades, decking, flashing, siding elevations, gutters, and interior water damage. |

| What is the homeowner’s strongest evidence? | A documented claim file: photos, estimate, code notes, storm date, mitigation records, carrier communications, and unpaid supplemental scope. |

What 215 ILCS 5/155 Says in Plain English

215 ILCS 5/155 is the Illinois statute homeowners and attorneys often reference when an insurance company allegedly delays, denies, or underpays a covered claim in a way that is vexatious and unreasonable.

The statute applies in an action by or against an insurance company where the dispute involves one or more of the following:

- The insurer’s liability under the policy.

- The amount of loss payable under the policy.

- An allegedly unreasonable delay in settling the claim.

When the court finds the insurer’s action or delay was vexatious and unreasonable, the court may allow reasonable attorney fees, other taxable costs, and an additional statutory penalty.

For homeowners dealing with storm restoration, this means the issue is not simply whether the insurance estimate was low. The real question is whether the carrier had a reasonable basis for its position and whether it handled the claim fairly based on the available evidence, policy language, damage documentation, and applicable building requirements.

Official statute: 215 ILCS 5/155

Why §155 Matters After Illinois Storm Restoration Claims

Storm damage claims in Illinois frequently involve more than replacing a few shingles. A complete restoration claim may include roofing, siding, gutters, fascia, soffit, windows, interior water damage, insulation, decking, flashing, ice barrier, ventilation, permits, code-required work, and emergency mitigation.

When a carrier writes a partial estimate that does not match the documented damage or code-compliant repair scope, the homeowner may face a serious financial gap.

Common Illinois storm restoration disputes include:

- Hail damage denied as “wear and tear” without a clear explanation.

- Wind damage minimized to isolated shingle repairs when full-slope replacement may be required.

- Siding elevations underpaid despite visible hail impact or discontinued materials.

- Gutters, downspouts, soft metals, fascia, or window wraps omitted from the estimate.

- Interior water damage excluded even though roof openings or storm-created damage caused leakage.

- Emergency tarping or mitigation invoices delayed or denied.

- Code-required items rejected without addressing the local building code or adopted code edition.

- Supplemental estimates ignored for weeks or months.

- Undisputed amounts delayed while disputed items remain under review.

A low estimate alone does not prove a §155 claim. But when the homeowner’s file shows repeated delay, unsupported denial, failure to investigate, or refusal to address documented damage, the claim may require attorney review.

Illinois Case Law Homeowners Should Know

Illinois courts have repeatedly stated that §155 is not a penalty for every coverage dispute. It is a remedy for insurer conduct that is vexatious and unreasonable.

The following cases are commonly cited in Illinois insurance disputes. These summaries are general and should be verified by counsel before use in litigation.

Cramer v. Insurance Exchange Agency, 174 Ill. 2d 513, 675 N.E.2d 897 (1996)

Key point: Illinois does not generally treat every alleged “bad faith” claim handling dispute as a separate tort. Section 155 provides an important statutory remedy for insurer conduct that is vexatious and unreasonable. However, a separate tort may exist only when the insurer’s conduct independently supports that separate cause of action.

Why it matters for storm restoration: Homeowners should not assume that “bad faith” is automatically a separate lawsuit. In Illinois, storm insurance disputes often require analysis under 215 ILCS 5/155, breach of contract principles, the policy language, and the claim record.

Scholar search:

https://scholar.google.com/scholar?q=Cramer+v.+Insurance+Exchange+Agency+174+Ill.+2d+513

Citizens First National Bank of Princeton v. Cincinnati Insurance Co., 200 F.3d 1102, 1110 (7th Cir. 2000)

Key point: Courts evaluate vexatious and unreasonable conduct based on the totality of the circumstances. A bona fide dispute about coverage can weigh against §155 penalties.

Why it matters for storm restoration: If the carrier has a reasonable dispute about causation, policy terms, or the amount of covered damage, §155 penalties may not apply. But if the carrier ignores evidence, delays without justification, or refuses to evaluate documented storm damage, the homeowner may have stronger grounds to seek legal review.

Scholar search:

https://scholar.google.com/scholar?q=Citizens+First+National+Bank+of+Princeton+v.+Cincinnati+Insurance+Co.+200+F.3d+1102

McGee v. State Farm Fire & Casualty Co., 315 Ill. App. 3d 673, 734 N.E.2d 144 (2d Dist. 2000)

Key point: The existence of a legitimate dispute can prevent a finding that the insurer acted vexatiously and unreasonably.

Why it matters for storm restoration: A homeowner should focus on building a factual record. The more complete the documentation, the harder it becomes for a carrier to claim the dispute was simply a difference of opinion.

Scholar search:

https://scholar.google.com/scholar?q=McGee+v.+State+Farm+Fire+Casualty+315+Ill.+App.+3d+673

Korte Construction Co. v. American States Insurance, 322 Ill. App. 3d 451, 750 N.E.2d 764 (5th Dist. 2001)

Key point: Courts may consider the insurer’s attitude, whether the insured was forced to sue to recover, and whether there was a bona fide dispute about coverage.

Why it matters for storm restoration: If a homeowner is forced to hire professionals, submit repeated documentation, and pursue legal action to recover amounts owed for a covered storm loss, those facts may be relevant to a §155 analysis.

Scholar search:

https://scholar.google.com/scholar?q=Korte+Construction+Co.+v.+American+States+Insurance+322+Ill.+App.+3d+451

What “Vexatious and Unreasonable” Can Look Like in a Storm Claim

The phrase vexatious and unreasonable is fact-specific. It does not mean the insurance company must agree with every contractor estimate. It also does not mean the homeowner wins a §155 claim simply because the final repair cost is higher than the carrier’s first estimate.

In storm restoration disputes, the strongest warning signs may include:

| Carrier Conduct | Why It May Matter | Documentation Homeowners Should Keep |

|---|---|---|

| Long delays without explanation | Delay is directly relevant under §155 | Email chains, claim portal messages, call logs |

| Failure to pay undisputed amounts | The carrier may owe some benefits even while disputing others | Estimate comparisons, payment ledger, carrier letters |

| Ignoring contractor supplements | A documented supplement should be reviewed in good faith | Supplemental estimate, photos, measurements, line-item notes |

| Rejecting code-required items without code analysis | Code compliance may affect the actual cost of repair | Local code citations, permit requirements, inspection notes |

| Denying hail or wind damage without reasonable investigation | Investigation quality matters | Roof photos, test squares, collateral damage, storm reports |

| Repeatedly changing denial reasons | Inconsistent reasoning may support attorney review | All denial letters, emails, adjuster notes |

| Misstating policy language | Policy interpretation must be grounded in the actual contract | Certified policy copy, endorsements, exclusions |

| Refusing reinspection despite new evidence | New evidence should usually be evaluated | Date-stamped photos, engineer reports, contractor report |

The strongest §155 files are organized, chronological, and evidence-driven.

The AOC Perspective: What Homeowners Should Understand Before Signing an Assignment of Claim

In restoration work, AOC often means Assignment of Claim or a similar assignment document connected to insurance proceeds. The exact legal effect depends on the language of the document, the policy, Illinois law, and the facts of the claim.

From a contractor’s perspective, an AOC may help document the relationship between the homeowner, the contractor, the scope of work, and insurance proceeds. But an AOC does not turn a contractor into the homeowner’s attorney. It also does not allow a contractor to make legal conclusions about bad faith or to practice public adjusting without the proper license.

For homeowners, the practical question is this:

Does the AOC clearly explain what rights are being assigned, what work is being performed, how insurance payments will be handled, and what happens if the carrier disputes the claim?

Before signing an AOC, homeowners should understand:

- Whether the document assigns only payment rights or broader claim rights.

- Whether the homeowner remains responsible for deductibles, upgrades, or uncovered work.

- Whether the contractor may communicate with the carrier about scope and pricing.

- Whether the contractor is attempting to negotiate coverage, which may raise public adjuster licensing concerns.

- Whether any §155 rights, attorney-fee claims, or penalties are affected by the assignment.

- Whether the homeowner should have an attorney review the document before signing.

A properly documented contractor file can support the homeowner’s claim. But only a licensed attorney should advise whether the carrier’s conduct supports a §155 claim.

What Contractors Can Document Without Giving Legal Advice

A storm restoration contractor should not tell a homeowner, “Your insurance company committed bad faith.” That is a legal conclusion. Instead, the contractor can document objective facts that may later help the homeowner, public adjuster, or attorney evaluate the claim.

Contractor Documentation That Helps a §155 Review

A strong storm restoration file should include:

1. Date of loss and storm verification

Use the reported storm date, weather records, NOAA data, hail maps when available, and photos of collateral damage.

NOAA Storm Events Database:

https://www.ncei.noaa.gov/access/search/data-search/storm-events

2. Damage photos by area

Photos should identify roof slopes, siding elevations, gutters, fascia, windows, soft metals, interior rooms, attic conditions, and water intrusion points.

3. Measurements and diagrams

Include roof measurements, siding elevations, gutter lengths, room dimensions, moisture maps, and affected material quantities.

Geospatial Intelligence, Aerial Imagery and Data | Eagleview US

4. Code and permit notes

Storm restoration may involve local building code requirements. In Illinois, code enforcement varies by municipality. Chicago, Cook County suburbs, collar counties, and downstate jurisdictions may follow different adopted code editions and amendments.

5. Itemized estimate

The estimate should explain labor, materials, waste, access, detach and reset, flashing, drip edge, ice barrier, ventilation, underlayment, decking, siding accessories, gutters, interior finishes, and mitigation.

6. Supplement explanation

Every supplemental line item should connect to a photo, measurement, code issue, manufacturer requirement, or field condition.

7. Communication timeline

Keep a clean log showing when the claim was opened, when inspections occurred, when estimates were submitted, when the carrier responded, and what remains unpaid.

This type of documentation does not accuse the carrier of bad faith. It simply creates a factual record.

Building Code Compliance Can Be the Difference Between a Low Estimate and a Proper Restoration Scope

Storm restoration is not just cosmetic repair. A repair must comply with the policy, manufacturer requirements, and local building codes. When an insurance estimate omits required items, the homeowner may not be able to complete a lawful or durable repair for the amount paid.

Common code-related issues in Illinois storm restoration include:

- Ice barrier requirements.

- Drip edge requirements.

- Roof deck condition and fastening.

- Flashing replacement.

- Ventilation requirements.

- Permit requirements.

- Re-roof limitations.

- Siding, sheathing, and water-resistive barrier details.

- Electrical or mechanical detach/reset requirements.

- Interior water damage and mold-prevention protocols.

Local code matters. A storm restoration claim in Chicago may not be evaluated the same way as a claim in Naperville, Aurora, Joliet, Rockford, Peoria, Springfield, Waukegan, Elgin, or a smaller Illinois municipality. A contractor should identify the applicable local requirements instead of assuming one statewide rule applies to every project.

For §155 purposes, code documentation may become important if the carrier rejects required work without addressing the code basis for the line item.

The International Building Code – ICC

Example: How a Hail Damage Roof Claim Can Become a Carrier Dispute

A homeowner in the greater Chicago area reports hail damage after a severe storm. The insurance carrier inspects the roof and pays for a few shingle repairs, a small gutter allowance, and no code-related items.

The contractor later documents:

- Hail impacts on multiple roof slopes.

- Collateral damage to gutters, downspouts, window wraps, and soft metals.

- Brittle shingles that cannot be repaired without causing further damage.

- Discontinued or non-matching materials.

- Flashing and ventilation items needed for a proper roof replacement.

- Local permit and code requirements.

- Interior water staining connected to storm-created openings.

The contractor submits a supplement with photos, measurements, and code notes. The carrier does not respond for an extended period, rejects the supplement without explanation, or repeatedly asks for documents already provided.

At that point, the homeowner may ask an attorney to review whether the carrier’s conduct is merely a legitimate dispute or whether it may be vexatious and unreasonable under 215 ILCS 5/155.

What Homeowners Should Do Before Accusing an Insurance Carrier of Bad Faith

Homeowners should avoid making emotional accusations. A stronger approach is to build the record.

Step 1: Request the Full Policy

Ask for a complete certified copy of the policy, including declarations, endorsements, exclusions, limitations, and ordinance or law coverage.

Step 2: Get the Carrier Estimate in Writing

Do not rely only on verbal statements from the adjuster. Request the carrier’s estimate, coverage letter, denial letter, engineer report, photo report, or claim notes where available.

Step 3: Ask for the Reason for Each Denied Item

If roof slopes, siding elevations, gutters, or interior damage are denied, ask the carrier to identify the policy basis, factual basis, and inspection basis.

Step 4: Submit a Complete Contractor Supplement

A supplement should not simply say, “Carrier estimate is too low.” It should show why the scope is incomplete.

Step 5: Track Time

A §155 review often depends on dates. Save every email, letter, text message, claim portal update, inspection notice, and payment record.

Step 6: Consult the Right Professional

Depending on the dispute, the homeowner may need a licensed public adjuster, engineer, building consultant, or Illinois insurance attorney. Contractors can document damage and repair scope, but legal advice should come from counsel.

Homeowners may also file a consumer complaint with the Illinois Department of Insurance:

https://idoi.illinois.gov/consumers/file-a-complaint.html

What §155 Is Not

Section 155 is powerful, but it is often misunderstood.

§155 Is Not Automatic

A denied claim, delayed claim, or underpaid claim does not automatically prove vexatious and unreasonable conduct.

§155 Is Not a Replacement for the Policy

The homeowner still must prove coverage, damages, policy compliance, and the amount owed.

§155 Is Not a Contractor Collection Tool

A contractor should not use §155 language to pressure a homeowner or carrier. Legal remedies belong in legal hands.

§155 Is Not the Same as Appraisal

Appraisal may resolve the amount of loss if the policy allows it and the dispute is appropriate for appraisal. Section 155 focuses on insurer conduct. An appraisal award may be relevant, but it does not automatically prove bad faith.

§155 Is Not Proof That Every Low Estimate Is Wrongful

Insurance estimates can differ because of pricing databases, measurements, repair methodology, depreciation, deductibles, exclusions, or coverage positions. The question is whether the carrier acted reasonably based on the facts and policy.

Questions Homeowners Should Ask an Illinois Insurance Attorney

A homeowner facing a serious storm restoration carrier dispute should ask counsel:

- Does the claim involve a bona fide dispute, or does the carrier’s conduct appear vexatious and unreasonable?

- Has the carrier paid all undisputed amounts?

- Did the carrier reasonably investigate the claimed hail, wind, water, or structural damage?

- Did the carrier address code-required restoration items?

- Are appraisal, breach of contract, declaratory judgment, or §155 remedies available?

- Does the policy include ordinance or law coverage?

- Does an AOC affect the homeowner’s rights?

- Are attorney fees, taxable costs, or statutory penalties available under 215 ILCS 5/155?

- Has the statute of limitations or policy suit limitation period become an issue?

- Should the homeowner file a complaint with the Illinois Department of Insurance?

Illinois §155 Storm Restoration Bad Faith Claims

Illinois homeowners searching “is my insurance company acting in bad faith after storm damage?” should know that Illinois commonly analyzes these disputes under 215 ILCS 5/155. Section 155 may apply when an insurer’s delay, denial, or underpayment is vexatious and unreasonable. In storm restoration claims, this can involve ignored supplements, delayed payments, failure to investigate hail or wind damage, refusal to address code-required repairs, or unsupported denial of roofing, siding, gutter, or water damage scope. But a legitimate coverage dispute is not automatically bad faith. Homeowners should document the full claim file and consult an Illinois insurance attorney before alleging §155 misconduct.

FAQ: Illinois §155 Bad Faith Claims After Storm Damage

What is 215 ILCS 5/155?

215 ILCS 5/155 is an Illinois Insurance Code provision that allows a court to award attorney fees, taxable costs, and a statutory penalty when an insurance company’s conduct or delay is vexatious and unreasonable in a dispute involving policy liability, the amount of loss, or settlement delay.

Is §155 the same as bad faith?

Homeowners often call it “bad faith,” but Illinois courts usually analyze insurer claim misconduct through the statutory language of vexatious and unreasonable conduct under §155. Illinois law does not treat every insurance dispute as a separate bad-faith tort.

Can §155 apply to hail damage claims?

Yes, it can apply to hail damage claims if the facts support it. A hail claim may raise §155 concerns if the carrier unreasonably delays, denies, or underpays covered damage after receiving proper documentation. A legitimate dispute about hail damage, age, wear, causation, or scope may defeat a §155 claim.

Can §155 apply to wind damage claims?

Yes. Wind damage disputes may involve missing shingles, creased shingles, lifted shingles, interior leaks, roof openings, siding damage, gutters, fascia, and emergency mitigation. The key issue is whether the carrier’s position was reasonable based on the evidence and policy.

Can a contractor say my insurance company acted in bad faith?

A contractor can document facts, damage, scope, code issues, and pricing. A contractor should not give legal advice or make final legal conclusions about bad faith. Homeowners should consult an Illinois insurance attorney for §155 advice.

What evidence helps a §155 claim?

Helpful evidence may include photos, videos, storm reports, contractor estimates, engineer reports, code citations, permit requirements, moisture readings, mitigation invoices, carrier letters, claim notes, email chains, and a timeline of delays.

Does a low insurance estimate prove bad faith?

No. A low estimate does not automatically prove bad faith or vexatious conduct. The issue is whether the carrier had a reasonable basis for its estimate and whether it handled the claim fairly.

What if the insurance company ignores my contractor’s supplement?

A single delay may not prove §155 conduct, but repeated failure to respond to a documented supplement can become important. Homeowners should keep proof of when the supplement was submitted, what it included, and how the carrier responded.

Can I file a complaint with the Illinois Department of Insurance?

Yes. Homeowners may file a consumer complaint with the Illinois Department of Insurance. A DOI complaint is not the same as a lawsuit and does not replace legal advice, but it may help document the dispute.

Complaint page:

https://idoi.illinois.gov/consumers/file-a-complaint.html

Should I hire a public adjuster, attorney, or contractor?

Each professional has a different role. A contractor documents repair scope and performs restoration work. A public adjuster may assist with claim adjustment if properly licensed. An attorney provides legal advice and evaluates §155, breach of contract, appraisal, and litigation options.

Final Takeaway for Illinois Homeowners

If an Illinois storm restoration claim is delayed, denied, or underpaid, the homeowner should not immediately assume the carrier acted in bad faith. The better approach is to build a clean, factual claim file and determine whether the insurance company’s conduct was reasonable under the policy, the damage evidence, the repair scope, and applicable code requirements.

215 ILCS 5/155 can be an important remedy when carrier conduct is vexatious and unreasonable. But the strongest claims are built on documentation, not frustration.

A qualified restoration contractor can help identify storm damage, prepare a code-aware repair scope, document the loss, and explain what is needed to restore the property correctly. An Illinois insurance attorney can determine whether the facts support a §155 claim.

For immediate service or consultation, you may contact us at Allied Emergency Services, INC.

Contact Information:

Phone: 1-800-792-0212

Email: Info@AlliedEmergencyServices.com

Location: Serving Illinois, Wisconsin, and Indiana with a focus on the greater Chicago area.

If you require immediate assistance or have specific questions, our human support is readily available to help you.

About the Author

Curt Testa is Owner and CEO of Allied Emergency Services, Inc., an Illinois-licensed storm damage restoration and roofing contractor serving Illinois and Wisconsin. With 27 years of field experience in storm restoration, insurance claim documentation, and code-compliant property repair, Curt has worked extensively on the contractor side of complex insurance disputes — including matters involving 215 ILCS 5/155 carrier conduct, Assignment of Claims contracts, scope and supplement disputes, and code-required restoration line items routinely contested by carriers.

Curt holds Illinois Roofing Contractor License #104.019029 (Qualifier and qualifying party, no disciplinary history), Wisconsin Dwelling Contractor Qualifier #DCQ-092100962, EPA Lead-Safe Certified Renovator credentials, OSHA 10 and 30-Hour Construction Safety certifications, HAZWOPER 40-Hour certification, FEMA emergency management training (ICS-100, ICS-200, IS-700 NIMS, IS-800 National Response Framework, IS-2900 National Disaster Recovery Framework, IS-552, IS-288, IS-559), and NWS SKYWARN Storm Spotter certification.

Allied Emergency Services is an IICRC Certified Restoration Firm (#70133670), EPA Lead-Safe Certified Firm (#NAT-F303832-1), and Vinyl Siding Institute Certified Installer (#28216). The company has operated under an Assignment of Claims model in Illinois and Wisconsin since 1997 and is BBB A+ Accredited.

This article reflects Allied Emergency Services’ analysis of 215 ILCS 5/155 and Illinois case law affecting storm restoration carrier disputes. It is not legal advice. Homeowners considering whether the facts of their specific claim support a §155 cause of action should consult an Illinois insurance attorney. Contractors evaluating their own operational practices in light of Illinois public adjuster licensing requirements should obtain advice from counsel familiar with the Illinois Insurance Code, including Power Dry of Chicago, Inc. v. Bean, 2022 IL App (2d) 210043.

Disclaimer: This article is intended for informational purposes only. For professional advice, consult experts in the field.

⚡ Storm or Roof Damage? Get a FREE Estimate

Text ESTIMATE to (844) 907-2546

Or call (800) 792-0212 for 24/7 emergency response

AI-powered • No obligation • Licensed IL & WI

Need insurance restoration help?

Allied Emergency Services — Licensed IL & WI Insurance Restoration Specialists

For 27 years, Allied has been handling insurance restoration across Illinois and Wisconsin. IICRC-certified, EPA Lead-Safe, IL Licensed Roofing Contractor #104.019029. 24/7 emergency response.

Learn about our Insurance Restoration service →Free property assessment within 24 hours · No obligation · Insurance claim support